Rynoh Pulse

Housing Forecast

April 2026 Updates

2026 Home Sales

2027 Home Sales

MBA Mortgage Origination

Refinance: +9.4% (2.20M vs. 2.01M)

Refinance: -10.3% (1.98M vs. 2.20M)

Overview

What does the April 2026 housing forecast mean for closing volume and escrow activity this year?

March housing data signals a clear seasonal acceleration — and for settlement agents, title underwriters, and closing attorneys, that means transaction pipelines are beginning to fill. Staying ahead of volume shifts is critical for managing escrow compliance, staffing, and underwriting exposure.

Existing home sales for March 2026 totaled 327,000 (non-seasonally adjusted), up +26.3% from February (February revised to 259,000) and +3.8% YoY, according to the National Association of Realtors (NAR). The spring buying season is underway, and closing desks are beginning to feel it.

Inventory is also rising. Active listings reached 1.23 million homes in March, up +9.5% from February and +4.2% YoY, marking the 28th consecutive month of annual inventory gains, according to Zillow. More listings moving to contract means more title searches, more commitments to issue, and more closings to coordinate.

Timelines are tightening. The median time to go pending dropped to 19 days in March, 9 days faster than February. For closing attorneys and settlement agents, compressed contract-to-close windows increase pressure on title production, escrow funding, and disbursement accuracy.

Home prices remain stable with regional variation. The national median existing home price was $408,800, up +1.4% YoY. The Northeast (+5.7%) and Midwest (+4.9%) are leading gains, while the South (+0.8%) is nearly flat and the West declined -1.3%. These regional trends directly influence premiums, liability exposure, and underwriting risk assessments.

Mortgage rates remain in the low-to-mid 6% range. Fannie Mae projects 6.2% in 2026 and 6.1% in 2027; MBA forecasts 6.1%–6.3%. Rates have stabilized enough to sustain purchase demand — keeping title and escrow activity elevated heading into the heart of the spring season.

Schedule a Demo

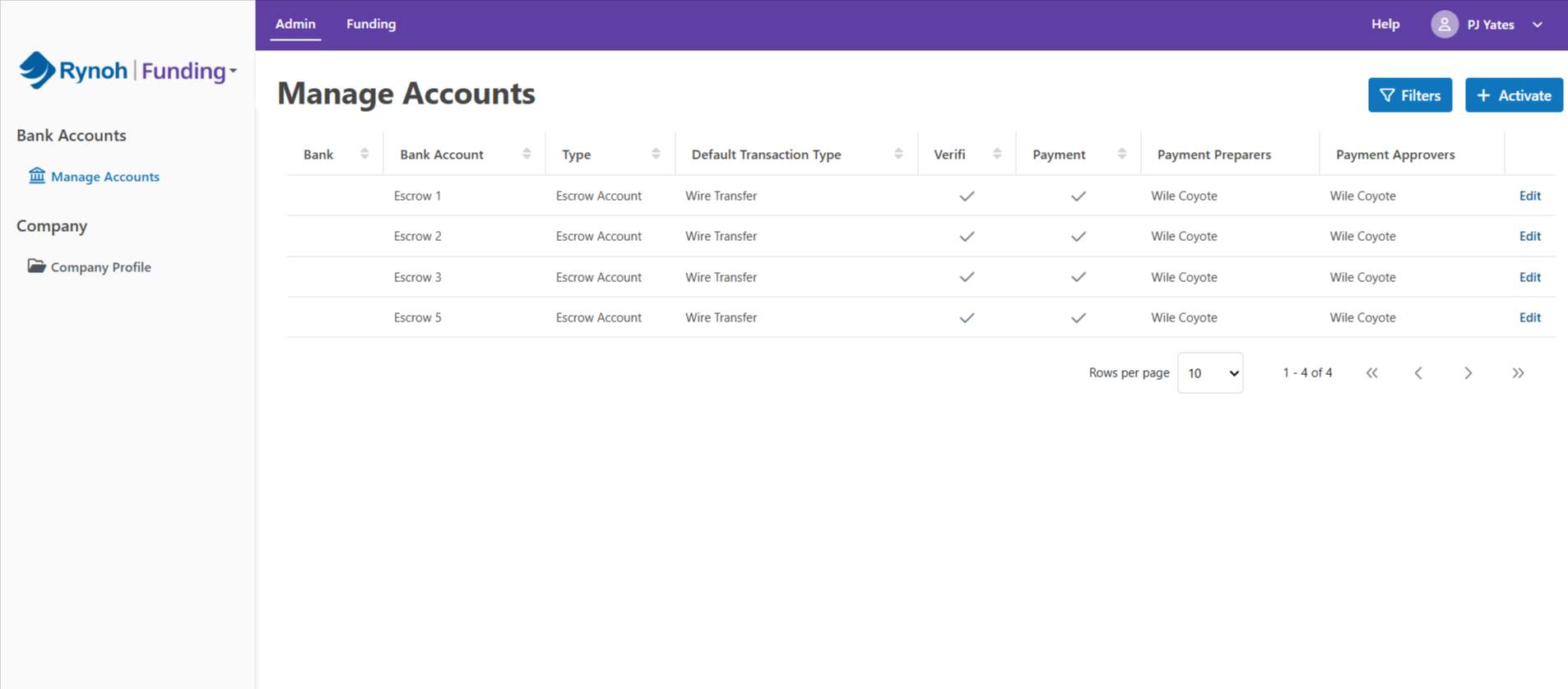

Rynoh performs daily audits and delivers detailed reports to ensure accuracy, compliance, and actionable insights for informed decision-making and improvement.

Escheat Professional Services

Connect Your Accounts.

Seamlessly integrate your accounting, escrow, and banking systems with Rynoh.

Forecasts for 2027 Home Sales (April ’26 forecast)

- MBA: +6.1% (5.23 million total home sales vs. 4.93 million) – April ’26 forecast

- Fannie: +7.6% (5.17 million total home sales vs. 4.80 million) – April ’26 forecast

MBA Forecast for Mortgage Originations (April ’26 forecast)

- 2026 Total Mortgage Originations: +5.5% (5.76 million loans vs. 5.46 million)

- Purchase: +3.1% (3.55 million loans vs. 3.45 million)

- Refi: +9.4% (2.20 million vs. 2.01 million)

- 2027 Total Mortgage Originations: -0.4% (5.73 million loans vs. 5.76 million)

- Purchase: +5.7% (3.76 million loans vs. 3.55 million)

- Refi: -10.3% (1.98 million vs. 2.2 million)

For settlement operations and underwriting teams, this is where capacity planning becomes critical. The projected increase in purchase originations — combined with a significant refi spike in 2026 — means closing volume will build steadily through the year. Firms that have automated escrow reconciliation, audit trails, and disbursement controls in place will be better positioned to scale without adding compliance risk. As transaction velocity increases and timelines shorten, the margin for manual error narrows. Now is the time to ensure your systems, workflows, and oversight processes are ready.