Release Date: 09.07.22

Author: P.J. Yates

The next phase of the digital payment revolution is being sought by businesses and organizations, driven by consumer demand for speed and convenience. The Real-Time Payment (RTP) network delivers real-time payments 24 hours a day, seven days a week, 365 days a year.

The Clearing House’s RTP network was established in 2017 and rapidly adopted by several banks. In 2020, the global pandemic presented a major payments disruption that caused many businesses to finally adopt the innovative faster payment solutions offered by The Clearing House.

The adoption of contactless payments has immensely boosted consumer usage of digital payment technologies. Consumers’ demand for quicker, contactless digital options from technology-forward service providers was obvious. Since then, the discussion in the U.S. payments ecosystem has focused on providing increased speed, more choices, and easier ways to send and receive money, which RTP provides to businesses.

RTP Overview

RTP is a payment method that outdated traditional methods like wiring or paper checks. With RTP, you can make and receive payments at any day or time – even including weekends and holidays! RTP transactions happen immediately, so payments can be done “just-in-time,” without worrying about losing float revenue.

What is RTP?

RTP is a payment solution developed by the Federal Reserve to increase the efficiency of payments in the United States. It allows for immediate settlement of transactions and can be used for B2C, B2B, and C2B models. RTP is available for companies and individuals that bank with an institution on the RTP network.

RTP reduces the number of needed steps in a process by adhering to the ISO 20022 standard and also allows for two-way data communication. RTP payments can be used for transactions that are worth up $1 million, whether they are standalone payments or Requests for Payment (RfP).

What is RfP in RTP?

RFP (Request for Payment) is a digital method of requesting cashback through the RTP network with almost instant settlement. This is useful for both one-time and recurring payments, subscriptions, and vendor/partner invoices or consumer charges.

RfP makes it easy to transfer money anytime, any day with little to no processing or reconciliation time needed.

How RTP works in real-time

The Real-Time Payments (RTP) network was created to operate at the speed of the digital economy. It’s available for immediate billing and payment, 24 hours a day, 7 days a week, 365 days a year.

Register For Webinar: X’s & O’s Playbook to Effectively Implement Automation into your Operations

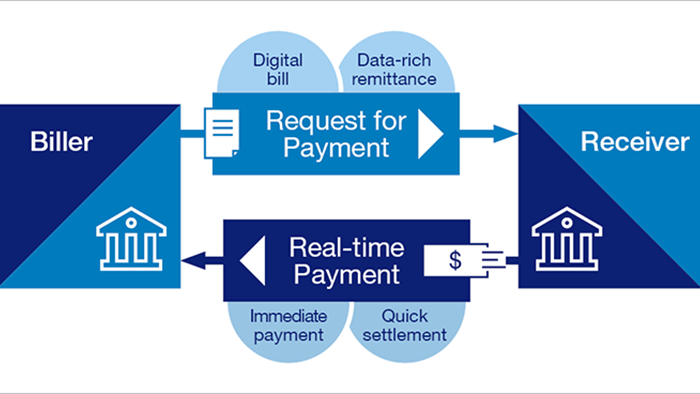

In a B2B transaction, the RFP through the RTP workflow processes payments in the following steps:

- The biller initiates a request for payment through their online banking application.

- The biller’s bank validates that the receiver’s bank accepts RTP and routes the request for payment to the receiver’s online banking application over the RTP network.

- The receiver verifies they want to pay and sends the payment back through their app.

- The RTP network validates the receiver’s payment.

- The RTP network sends the payment to the biller’s app.

- Confirmation of the payment is provided back to the receiver’s app.

After establishing your offer and the buyer accepts, you will submit an RFP. This process results in a cash advance right away. A food supplier might send an RfP when unloading a delivery at a restaurant, for example. The bill may be paid with one click that is immediately verified.

Catching up with the real speed of business

The average RTP transaction takes only a few seconds to process, rather than the standard one or two days for an ACH transaction. This saves time and money compared to other methods like checks.

But catching up doesn’t have to do with just speed. The value means meeting customer expectations and creating efficiency in money movement. As RTP has evolved, certain scenarios have emerged when real-time really makes a difference for businesses, such as:

- Deliver urgent payments to customers immediately (e.g., insurance claims)

- Manage recurring monthly payments efficiently (e.g., utilities, gym memberships, cell phone bills)

- Send follow-up requests for NSF items (e.g., returned ACH payments)

- Enable control and pay bills with precision (e.g., on due dates)

What this means for treasury professionals

In the first-ever payment, U.S. Bank was one of the first banks to operate on the RTP network and took part in the initial transaction. In 2019, US Bank opened all routing numbers for real-time payments with messaging functionality.

According to The Clearing House, there is still great potential for RTP with 70% of businesses planning to adopt it within the next two years. Additionally, there are several practical applications for RfPs like using them as follow-ups for rejected checks or returned ACH payments. not only providing immediate value to companies but also allowing different payment options to work together cohesively.

for a long time, it was predicted that paper checks would slowly die out. Even though this is the case, many people still use them on occasion. In some business-to-business settings, digital payment methods are not an option for vendors and payers can’t send electronic remittance detail. To reduce check volume for these types of transactions and provide customers with the experience they expect from modern businesses, RTP may be a great solution.

The All-In-One Automated Teller Machine (AITM) is a Bitcoin ATM that allows users to digitally exchange their cash on deposit at an existing bank account for Bitcoins. The machine also acts as an RTP terminal, allowing you to receive inbound payments via SMS on your mobile phone. This is just one aspect of a complete payment plan. If you need assistance designing it, we have the tools to get you started.

Register For Webinar: X’s & O’s Playbook to Effectively Implement Automation into your Operations